This two-part series explores how race built the city of Memphis. First, we examine a redlining map from 1930s that government agencies and lenders used to facilitate discriminatory housing policies that kept Black families and neighborhoods from thriving. Part two dives deeper into the Opportunity Home Loan Fund and other efforts by South Memphis CDC The Works Inc. to bring investment back to Memphis' disinvested and historically Black communities.

On March 17, Massachusetts Senator and 2020 presidential candidate Elizabeth Warren met with community leaders in Memphis for a conversation on ways to rebuild the middle class, which is a key issue in her Democratic primary campaign.

Roshun Austin, president of South Memphis community development corporation

The Works Inc., attended the meeting and said she appreciated that Warren was willing to listen and learn. When Warren turned the conversation towards Black homeownership as a way to build wealth among Black families, Austin

set her straight.

Related: "Seeing Red II: South Memphis CDC brings investment back to Memphis' formerly redlined communities"

“I said, ‘Let’s just take that lie off the table.’

Study after study over the last 30 to 40 years has shown that’s not true,” said Austin.

Austin is an urban anthropologist with a 25-year career in nonprofit housing development in Memphis’ most disinvested neighborhoods. She also spent eight years in foreclosure prevention during the build up, crash and aftermath of the 2008 financial crisis.

She explained to Warren what community developers and most Black Americans have long known —

housing has been a tool to

suppress Black wealth, not grow it.

Across the Memphis metro area, the

poverty rate for Black Memphians is an estimated 24.5 percent compared to 8.1 for white Memphians. Despite an estimated 13,000 to 15,000 vacant houses in the city, Black homeownership dropped 18 percent from

2005 to

2017, putting Memphis in the top third of declining cities in the U.S.

Forty-two percent of Black Memphians own homes compared to 72 percent of white Memphians.

Most wealth is built by owning and inheriting property, but centuries of slavery, racism and racist policies have limited Black wealth, incomes and the credit and collateral necessary to access home ownership and the middle class.

Across the U.S., the average Black family

holds a tenth of the wealth of the average white family.

“I think people are in a cloud sometimes to think that we’ve made way more advancement than

we’ve actually made,” said Austin.

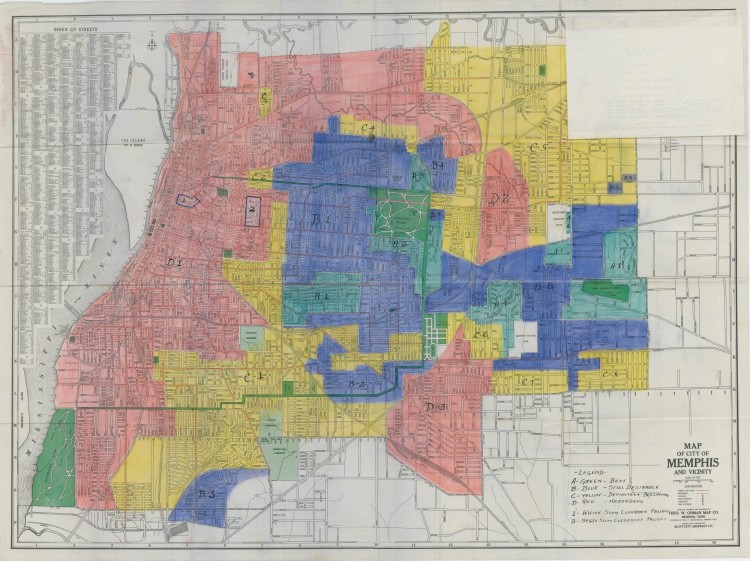

It’s a complex history that can be difficult to navigate, but luckily, there’s a map.

It’s a redlining map from the 1930s unearthed two years ago from the National Archives and Records Administration by researchers at the University of Richmond’s

Digital Scholarship Lab. It and others like it were used until the late 1960s to designate neighborhoods as safe (blue and green), moderately risky (yellow) or unsafe (red) for mortgage and construction lending.

With few exceptions, redlined neighborhoods were majority-minority while greenlined neighborhoods were exclusively white. Yellow often buffered the green and blue from the red.

![]() A redlining map of Memphis drawn in the 1930s by the Home Owners' Loan Corporation. (National Archives and Records Administration)

A redlining map of Memphis drawn in the 1930s by the Home Owners' Loan Corporation. (National Archives and Records Administration)

With the maps as a guide, federal and local governments worked with banking and insurance industries to develop practices and policies that undermined Black wealth at the neighborhood level by gutting investments and concentrating poverty in redlined communities.

Austin Harrison, program manager for Memphis-based nonprofit Neighborhood Preservation Inc., said the Memphis map is a sort of holy grail for local community leaders — proof disinvestment was intentional.

“We’ve got to put that on the table and agree that this was not accidental,” said Harrison. “It wasn’t by accident, it wasn’t a byproduct of hodgepodge development. It was intentional, an intentional policy that was implemented holistically.”

Residents in “undesirable” neighborhoods like South and North Memphis saw

home values plummet. Builders, developers, business owners and residents with means followed the money to greener neighborhoods. The exodus was used as further evidence redlined neighborhoods were dangerous for investment.

It was the beginning of a 90 year cycle meant to maintain white wealth and social superiority.

“The program — the housing program, the urban programs — that this was a part of were very much about making sure white families had access to both public and private sources of capital and cutting neighborhoods of color off from those,” said Robert Nelson, director of the Digital Scholarship Lab, which is digitizing redlining maps from across the country.

But with proof comes the chance to have a more honest conversation about the vast ramifications of redlining on communities of color.

“Anyone can see how these neighborhoods that were redlined corresponds to current poverty rates, corresponds to vacant and abandoned properties, unbanked households, mortgage originations, health determinants, life expectancy,” said Harrison. “Name the social determinant, you’ll see that these areas were denied investment and capital and have been for decades and how that is playing out currently in the social environment of those neighborhoods.”

NPI, a nonprofit that addresses neighborhood and city-wide barriers to Memphis growth, is now partnering with Nelson and his team to incorporate a digitized version of the map into NPI’s

Property Hub database. It would allow community leaders to layer health, housing and other data onto the old map and see the current connections. Harrison said the goal is to give communities the tools needed for that honest conversation and the hard evidence needed to sway policy makers.

Meanwhile, Austin and The Works hope their Opportunity Home Loan Fund program will start a new conversation with lenders about their risk assessment practices. The program focuses on behaviors over credit score and collateral and targets loan opportunities in ZIP codes in the same neighborhoods redlined in the 1930s — North Memphis, South Memphis, Orange Mound and Binghampton.

“What I’m trying is an experiment to some degree to prove to local banks, even if big giant banks don’t listen to us, that these homeowners do pay,” she said. “These neighborhoods and these people are worth investing in. They are not going to be in default.”

"It's unfortunate that we have to prove those things ... but that’s America.”

Drawing Lines

The Memphis redlining map shows South Memphis, North Memphis and Downtown as a single swath of red. Patches of red also denoted Orange Mound and the east side of Binghampton.

Green and blue dominate the center city and follow the Poplar Corridor through the Medical District, Midtown, Vollintine-Evergreen and University District to the eastern city limits at Graham-Goodlett.

Yellow stretches east from North Memphis to The Heights and from South Memphis to the Fairgrounds.

“That map from the '30s was quite interesting because it doesn’t look too far from today,” said Austin. “It’s just that Memphis has expanded significantly since that map.”

For the remaining 20th century, redlining spread in waves as wealthy and middle class Memphians — most white but many Black — pushed further and further from the center city and lower income families followed, moving north, south and east along Poplar.

Between 1935 and 1940, the Federal Home Loan Bank Board

commissioned the Home Owners' Loan Corporation,

or HOLC, to produce a map for any U.S. city with 40,000 residents or more — over 240 cities in all. HOLC hired local lenders, insurers and real estate agents to draw the maps.

“These are evidence of the federal government’s role in this,” said Nelson. “It’s not just the marketplace that causes these great variances in wealth, it’s federal policy that does that.”

Nelson notes HOLC wasn’t the only agency creating these maps. In fact, HOLC created tutorials to teach others how to draft their own maps, but HOLC’s are likely the earliest in most cities and are by far the most extensive.

The

Mapping Inequality project — a partnership between the Digital Scholarship Lab, University of Maryland, Virginia Polytechnic Institute and State University and Johns Hopkins University — has

digitized maps and area descriptions for 150 cities so far and will soon add maps for three dozen cities, including Memphis.

The Digital Scholarship Lab expects to complete the digitized Memphis map by May 2019. High Ground News received an advance look at the draft map and will share the digital version as soon as it is available.

End of The Line?

Redlining was formally banned by the 1968 Fair Housing Act, but Austin said financial institutions have yet to change their underlying practices.

“In almost 100 years, as much as we want to believe that actions at the federal level by Congress and prior presidential administrations, even at the state and local level have changed redlining practices — the more things change, the more things stay the same,” she said.

Prior to the 2008 crash, lenders

disproportionately issued subprime and adjustable rate mortgages, inflated interest rates and other predatory practices in majority-minority neighborhoods. Black families faced underwater mortgages and foreclosures at rates higher than white families and lost a

higher percentage of their wealth because white families were more likely to have other assets to buffer the loss of a home.

According to the Federal Reserve, the

median wealth in 2016 for Black families including all assets and inheritance was $17,600 compared to $171,000 for white families.

South Memphis’ 38106 ZIP code has been one of the hardest hit in the country in terms of decreased home values and underwater mortgages. The 2018 U.S. Home Equity and Underwater Report from ATTOM Data Solutions shows more than 60 percent of mortgages in this South Memphis ZIP code are underwater.

“We find that neighborhoods like this, ZIP 38106, have the highest number of underwater mortgages, so how does that create wealth?,” said Austin.

In seven years, banks in Memphis have faced at least three major lawsuits for discriminatory lending. In 2012, Wells Fargo

settled for $432.5 million

for targeting Memphis' minority neighborhoods with predatory loans prior to the financial crisis. In 2016 First Tennessee

settled for $1.5 million for denying loans to qualified Black and Latino applicants and failing to put branches in minority neighborhoods in Memphis, Nashville, Chattanooga and Knoxville.

Also in 2016, BancorpSouth

settled for $10.6 million for denying and inflating loan prices for minority borrowers, failing to put

branches in minority neighborhoods and directing all of their marketing towards Memphis' majority-white neighborhoods.

Austin said while lawsuits bring attention, they’re essentially a slap on the wrist. In the

case of BancorpSouth

, $10.6 million dollars is

just over one percent of their annual revenue.

![]() Stray dogs walk the street in The Heights. The Heights experienced heavy white flight from the 1960s through the 1990s resulting in an estimated 1,100 vacant lots and houses. Stray dogs use abandoned properties as safe dens and are a symptom of those vacancies. (Natalie Eddings)

Stray dogs walk the street in The Heights. The Heights experienced heavy white flight from the 1960s through the 1990s resulting in an estimated 1,100 vacant lots and houses. Stray dogs use abandoned properties as safe dens and are a symptom of those vacancies. (Natalie Eddings) Shifting Cities

Redlining wasn’t wholly responsible for racially-based housing discrimination in 20th century America, but it was a catalyst.

In yellowlined neighborhoods, real estate agents and investors warned white homeowners their property values would disappear if more people of color moved in.

Known as blockbusting, agents would buy the homes at below value, perpetuating depreciation and scaring other white residents into leaving.

Blockbusting triggered the first wave of

white flight, the mass movement of the white middle class from cities to suburbs. In the 1940s and '50s,

white flight intensified when the Federal Housing Administration began underwriting 30-year mortgage loans. Soldiers returning from World War II could use the G.I. Bill for education and own a home thanks to the FHA.

It was

the advent of the suburbs and American middle class, and solidified homeownership as the new American Dream.

But across the country, developers listed new subdivisions as whites-only for a greenlined designation. Higher education was less accessible to people of color, and as wealthier whites left for the suburbs, they took the tax base

funding public K-12 schools with them.

White Memphians moved into East Memphis and northeast and southeast to Berclair, Raleigh, Frayser, and Whitehaven. Austin noted many white residents in the center city neighborhoods like Midtown and Vollintine-Evergreen stayed and those pockets are still wealthier and whiter today than much of the inner city.

Memphis shifted again as the Civil Rights Act of 1964 and Fairing Housing Act of 1968 formally ended redlining and Jim Crow segregation. Many white Memphians moved to farther suburbs and neighboring states and counties to escape integration of neighborhoods and schools and protect their property values.

Meanwhile, Black families who did have some wealth were no longer restricted by segregation and headed into formally majority-white neighborhoods like Frayser and Hickory Hill. Those neighborhoods then began to see the same lack of investment as other redlined neighborhoods while historically Black communities like South and North Memphis slipped further into decline.

Harrison noted most but not all families with means left their yellow or redlined neighborhoods, but he estimates there are currently 13,000 to 15,000 vacant homes and lots in Memphis as a result of the flight of the middle class.

With continued expansion of people and the city limits into the 21st century, individuals and companies took advantage of cheap stock in an over saturated market for rental investments.

Thirty-three percent of single-family homes in Memphis are rentals, and studies from data firm ATTOM Data Solutions show Memphis is a top U.S. market for flipping houses to rent.

Out-of-town investors are a major source of the city’s code violations, which further devalues disinvested neighborhoods. The

Memphis Blight Elimination Steering Team found in spring 2018 at least four of the top 10 code violators in Memphis were out-of-state companies.

NPI was key in launching the team, which has over 20 partner agencies, and uses its Property Hub database to

make blighted property data more accurate and accessible.

Austin said problem property owners are difficult to track, and with only 41 code officers in the City of Memphis, there’s little enforcement. The Works is supporting a city policy requiring out-of-town owners to have a responsible party living in Shelby County. The City of Memphis

hopes to have the property owners registry in place by 2020.

“Right now we’re serving ghosts,” said Austin. “As our tax base has eroded, we have a sparse city and a lot of delinquent properties.”

Beale Street and Urban Renewal

From 1949 until 1974,

urban renewal also played a major role in dismantling communities of color and much of Memphis’ Black upper and middle class. Under

urban renewal, city governments classified residents as blight and displaced them for new development.

In a recent On the Ground Podcast episode, Austin highlighted Beale Street’s transformation from epicenter of Memphis’ Black culture to tourist destination as a prime example of this intentional and destructive development policy.

Related: "On the Ground Podcast: Memphis' modern day redlining"

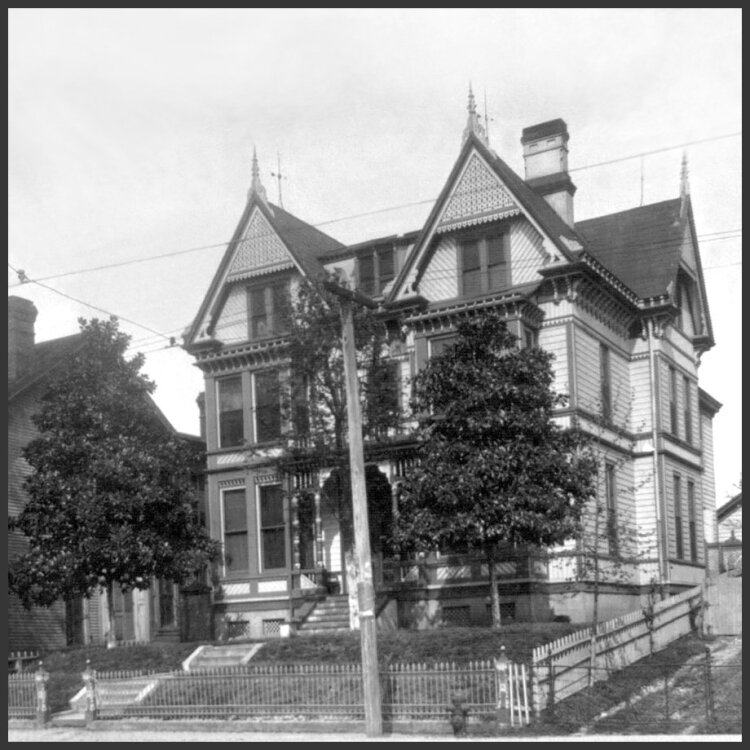

In

the early 19th century, Beale and the area surrounding its eastern end was an integrated neighborhood with a thriving upper and middle class Black community. Far from blighted, it had a strong professional class, Black-owned businesses, entertainment, schools and churches. It was also home to Black social and political leaders, including the Church family and their stunning Victorian mansion at 384 South Lauderdale Street.

Robert Church Sr. was a merchant, real estate investor and the South’s first Black millionaire. His son, Robert Church Jr., was at the epicenter of Black political power when redlining began.

![]() The Church family mansion once stood as a symbol of Black economic and political success in what is now being redeveloped as South City. The City of Memphis burned the mansion to the ground in 1953. (Library of Congress)

The Church family mansion once stood as a symbol of Black economic and political success in what is now being redeveloped as South City. The City of Memphis burned the mansion to the ground in 1953. (Library of Congress)

By the 1930s, there had been a 30 percent increase in the city’s Black population and a rise in its economic and political power. In response, the city government and Edward “Boss” Crump, who controlled the Memphis political scene from 1910 through the 1950s, launched a four-decade campaign to concentration Black residents into housing projects and away from economic opportunities in white, greenlined neighborhoods.

The city leveled the neighborhood southeast of Beale and immediately adjacent to the Church home to make room for

Foote Homes, the city’s only Black housing project. Then they bankrupted Robert Church, Jr., foreclosed on the mansion and let the Memphis Fire Department burn it to the ground in a show of political power in 1953. In 1955, the city opened Cleaborn Homes where the Church home once stood. More about this phase of Memphis urban renewal can be found in scholar Preston Lauterbach's 2016 article

"Memphis Burning".

Urban renewal continued on and around Beale until the mid-1970s. The Memphis Housing Authority displaced almost 800 individuals and families from the area.

Related: "The last major vestige of segregation-era housing set for demolition"

At the time, the segregation-era housing projects were branded as an opportunity for modern living and self-improvement. A 1940 Commercial Appeal article reporting the Foote Homes grand opening quoted U.S. Housing Authority representative Claude Parsons as saying:

“[Foote Homes is] built for you, your family and your children, and you must realize this and accept the opportunity for improvement. If you fail us, you will fail America in the end.”

Foote Homes and Cleaborn Homes were phased out and demolished by 2017. Much of the land is now being redeveloped as part of a $210 million South City Choice Neighborhoods grant from the U.S. Department of Housing and Urban Development. The development is intended to bring businesses, housing and economic and racial diversity back to the area.

Related: “As Downtown grows, South City invests in low-income residents”

Returning Investment

The Works’ Opportunity Home Loan Fund is a $2 million fund targeting nine ZIP codes in South Memphis, Orange Mound, Binghampton and North Memphis.

“We don’t look at [credit] scores necessarily, we look at behaviors,” said Austin

Things like regular rent and cell phone payments, even if they’ve been paid by money order, contribute to the borrower's profile.

The program launched in February 2017 and has issued 22 home loans of $50,000 or less. Initial funding came from a community investment tax credit through partner Pinnacle Financial Partners.

The loans are low interest, low down payment and are designed to keep borrowers from getting underwater. The program includes financial literacy training and a 10 percent surplus built into borrowers' budgets to ensure an emergency doesn’t spell disaster.

“I saw people that may have had some degree of wealth lose everything in the crisis. From the Rust Belt to California from New York to Florida, I was watching families experience this, so it informs how we underwrite loans,” said Austin. “I saw people fall behind because a tire went out on their car or [because] gas prices went up.”

![]() The Works, Inc. staff members pose for a photo with Roshun Austin standing center. The Works has a number of housing initiatives aimed at revitalizing Memphis' most disinvested neighborhoods. (Submitted)

The Works, Inc. staff members pose for a photo with Roshun Austin standing center. The Works has a number of housing initiatives aimed at revitalizing Memphis' most disinvested neighborhoods. (Submitted)

Austin said so far her rate of default is less than traditional lenders, and in a couple of years, she’s confident she’ll have irrefutable proof that low and moderate-income Black families can be successful borrowers when their unique needs and history are understood and respected.

It’s the same sort of proof Harrison hopes the map will provide in a conversation about inequality in Memphis and solutions to rectify it.

“What I hope the redlining maps do is provide perspective to the way we view space and we no longer think of space as a product of market,” he said. “I hope that at the very least, we can start a conversation about why these neighborhoods are like they are and the realities, not the perceptions.”

Austin said

media, scholars and the public are

increasingly focused on the U.S.’s history of racial discrimination. It’s a great time for the map to surface and Memphians to start a more frank conversation.

“It’s on television, it’s in the rhetoric,” she said. “It’s always existed for people who’ve been victim to it. But they couldn’t really get a voice and nobody was listening to them.”

Part two of this series will p dive deeper into The Works' many efforts, including the Opportunity Home Loan Fund. Check our website and social media for the latest or sign up for our weekly edition to have Seeing Red I and II delivered for free to your inbox.