If I drive in South Memphis, or North Memphis or Frayser, I see more pawn shops, more payday loans than anything. If I drive in Germantown, if I drive in Cordova, you have to have a magnifying glass to see one. They flash across the TV screens here. It's more in our neighborhood than other neighborhoods.

LaTonya Taylor is a South Memphian and former victim of predatory lending who now has a small business, a 401K and a savings account.

She is a success story, but, before participating in the RISE Foundation's financial literacy program, she was also part of the millions of Americans who are under or unbanked.

According to Bank on Memphis data, 40 percent of the Memphis Metro Area is unbanked or underbanked. That’s about 90,000 unbanked and 120,000 underbanked households.

Nationally, about 7 percent of people are unbanked, meaning they don't have a bank account, and another 20 percent are underbanked, meaning they may have a bank account but regularly use alternative financial services like payday loans, check-cashing storefronts that charge substantial fees and installment debt available with exorbitant interest rates.

Unbanked and underbanked rates are highest among lower-income households, less-educated households, younger households, black and Hispanic households, and working-age disabled households, according to data from the Federal Deposit Insurance Corporation.

It is unsurprising, then, that ZIP code 38126 in Memphis, which has a poverty rate nearly double of any other area of Memphis, is dotted with payday lenders.

There is only one bank, a lone SunTrust location that sits across from LeMoyne-Owen College and is only open Monday and Fridays from 9 to 2.

The area of ZIP 38126, which stretches from Third Street, Interstate-240, Martin Luther King Boulevard and McLemore Avenue is burdened with a 62 percent poverty rate. Seventy-three percent of the population has a high school education or less.

Some organizations, like the RISE Foundation, attempt to empower this vulnerable population with financial literacy.

![]() LaTonya Taylor, owner of Epic Bouncing, plants a sign in a client's yard while setting up a bounce house. She started her business with support from the RISE Foundation.

LaTonya Taylor, owner of Epic Bouncing, plants a sign in a client's yard while setting up a bounce house. She started her business with support from the RISE Foundation.

Linda Williams, president of the RISE Foundation, points to three factors that lead to the high numbers of unbanked people in the neighborhood and these sentiments echo through the stories of those who have lived unbanked and those who have popped up in organizations who seek to mitigate the problem.

They remain unbanked or underbanked because of accessibility, bad experiences and a generational mistrust and disuse of financial institutions.

The cycle

Although Rise, Advance Memphis, and the Women’s Foundation for a Greater Memphis all facilitate programs to teach financial literacy, residents of ZIP 38126 have legitimate reasons to stay unbanked.

An unbanked community is a cash-centered community, which both Williams and Ann Brainerd at Advance Memphis have noticed hinges more and more on prepaid debit cards. These cards can be bought at area stores and can be used to pay bills, withdraw cash at ATMs, make purchases, deposit checks and receive direct deposits.

Many employers may pay wages with these cards as a simple payroll solution to avoid banking or to accommodate undocumented or other off-book workers.

These cards often charge a fee for each transaction. While prepaid cards can offer mild security, card users often withdraw their cash all at once to avoid these fees, leaving the wages vulnerable to loss and theft. While these risks seem high compared to traditional banking, many cannot or do not believe they can meet the minimums often required to open a checking account.

“People don’t understand how bank accounts work. I hear the stories a lot where a check didn’t clear fast enough and, when they called for their balance, it was there and they spent it,” Williams said.

“They are not in the habit of expecting expensive overdraft fees. So, when people have a bad experience, they tend to stay away and use money orders. A lot of people in the neighborhood only accept money orders anyway, like landlords after people have written checks that bounced," Williams added.

![]() The boarded up storefront on Vance Avenue near Danny Thomas Boulevard most recently served as a corner store.

The boarded up storefront on Vance Avenue near Danny Thomas Boulevard most recently served as a corner store.

Unlike checks, however, money orders often come with up to $2 fees, which can add up to make-or-break sums over time.

Job and income volatility means many residents cannot keep enough money in the bank to keep the account open or to consistently pay bills using the account.

According to the FDIC survey, this is true nationally. Even among households with higher levels of income, unbanked and underbanked rates were higher when that income was volatile.

Taylor said that she did have a bank account before connecting the Rise, but she misused it. When she ran out of money and couldn’t wait until the next paycheck, she looked to what she learned from her mother to pay the bills.

Taylor, who now owns her own business, compares financial habits to eating habits. Taylor said that her mother, who grew up with very little food, let her children use their food stamps to purchase whatever they would like instead of imposing healthy eating habits. The example translates well with financial habits, Williams added.

“It’s cultural. It’s how you were reared and how you saw your parents use money. I’m breaking generations of curses and setting the tone for what I want for my own family,” said Taylor.

Interestingly, according to Brainerd, the demographics of Advance Memphis’ foundational 12-week financial literacy class, Faith & Finances, have shifted since those living in recently-closed public housing have been scattered around the city. While traditionally almost all of the program participants have been unbanked, she has seen a rise in those with some banking experiences.

Williams describes what Rise does as “breaking into the cycle.” She says that this is yet another generation of families in a long line of 38126 residents who have had negative experiences with traditional banking and passed on those habits to their children.

And residents have legitimate reason to be mistrustful. Poor black populations are the same ones that financial institutions have overtly discriminated against for generations through policies like redlining and subprime-credit targeting.

![]() LaTonya Taylor, of Epic Bouncing, and her son Michael, 3, fill up the pool of the bounce house while setting up in a client's yard.

LaTonya Taylor, of Epic Bouncing, and her son Michael, 3, fill up the pool of the bounce house while setting up in a client's yard.

ZIP 38126 is, after all, the same neighborhood that was a thriving middle-class black neighborhood built up and rented out by Robert Church, Sr. who founded a bank that catered to the African-American population. That was until the city, under the direction of Mayor E.H. “Boss” Crump, bulldozed ten blocks of the community in the late 1930s and turned it into public housing, the same Foote Homes that is only now being demolished. In its place will rise 712 units of mixed-income housing.

The FDIC found that households that feared being rejected for credit from banks or had previously been rejected were much more likely to turn to alternative lenders. Among the unbanked, more than half of respondents said that traditional banks weren’t at all interested in serving families like theirs.

Bank On Memphis is part of a national outreach effort targeting the unbanked and connecting them to banks that have low or no-cost checking or savings accounts with low fees and low minimums specifically offered to transition the unbanked to traditional financial institutions and help them maintain the accounts.

The program is described on its website as “a public-private partnership between the City of Memphis, Shelby County government, financial institutions and nonprofits to encourage the unbanked to establish an account at a mainstream financial institution.”

The free Bank On Memphis app has been downloaded more than 2,100 times and more than 6,500 bank accounts have been opened through their work.

The stopgaps

Despite the legitimate reasons that the unbanked choose to be so, it is undeniable that the alternative financial services like cash advancers, payday lenders, and auto-title operators prey on this instability and dramatically increase the price of being poor.

Although residents may prefer the fees they know in the large, neon poster print of cash advance fees to the unknown fee structure and fine print of a bank, the financial cost of using these services works out to an average loss of $2,500 per family each year just to access their own money or take out a loan, according to the FDIC.

.jpg)

![]() Linda Williams, president and CEO of RISE Memphis, stands for a portrait at the foundation's office.

Linda Williams, president and CEO of RISE Memphis, stands for a portrait at the foundation's office.

According to the federal Consumer Financial Protection Bureau, payday loans typically have an annual percentage rateas high as 390 percent; however, they market themselves a short-term solutions and most users don’t expect to pay interest over time.

Alternative financial services also cast themselves as saviors and friends of the community.

“Payday lenders say, ‘We provide what banks don’t because we’re in the neighborhood where banks aren’t,’” Williams said.

“But if you have no emergency savings and your car battery goes dead, you rather get a cash advance and pay up to 20 percent in fees than have no car.”

Before coming to Rise, LaTonya Taylor found herself in a similar situation. She took her car to a pawn shop when she couldn’t pay her bills and, after missing a payment, it was taken away.

“I remember taking my car to the pawn shop. They didn’t tell me the interest. Well, they quoted it, but it didn’t make sense to me. That was a huge problem for me,” Taylor said.

Brainerd cites Memphis, Light Gas & Water bills as the most common cause of emergency situations. Although she acknowledges that some people simply can’t pay and late payment allowances run out, she points to the practice of estimating bills as a major factor.

“They estimate the light bill and suddenly you have a big chunk to pay. When you’re already on a fixed or low income and you don’t have savings, you can’t just pay double what you thought you were gonna pay,” Brainerd said.

This cycle of dire financial emergencies and stopgaps that cost more long-term is the situation forced on low-wage or unemployed workers who live paycheck-to-paycheck, which is the vast majority of those living in 38126. Sixty-nine percent of residents are either unemployed or out of the labor force and not looking for work.

Of those who can find a job, they are almost exclusively low-wage jobs.

![]() Linda Williams flips through a folder of homes that have been purchased by folks with the help of RISE Memphis financial literacy programs.

Linda Williams flips through a folder of homes that have been purchased by folks with the help of RISE Memphis financial literacy programs.

Taylor, like many others, picks up “side hustles” to make enough extra money to be able to save. In addition to a position at Porter-Leath, she delivers papers for the Commercial Appeal and rents out water slides for events.

Alternative lenders take advantage of these circumstances and continue the cycle of poverty for many. However, several organizations in Memphis have stepped up to teach a better way.

Breaking the cycle

Both Williams and Brainerd say that those who have been using alternative financial services often mismanage their funds because they have never been taught ideal financial practices. Programs at Rise and Advance Memphis fill the education gap with relatable examples of how to improve financial habits.

Rise targets low-income populations through the Memphis area whereas Advance Memphis, situated on Vance Avenue, targets the 38126 area specifically and is faith-based.

Rise’s Common Sense program for workplaces, their Save Up program, and Advance’s Faith & Finances program are standard financial literacy programs that are specifically designed to use group discussion and relevant examples to make low-income Memphians feel comfortable.

The programs include education about what determines a credit score, which can be crucial as the additional cost of opening a utilities account or buying an asset increases if you have a low credit score. It also teaches them to log their spending habits to find where their money goes, how to shop smart and tips on how to save money long term.

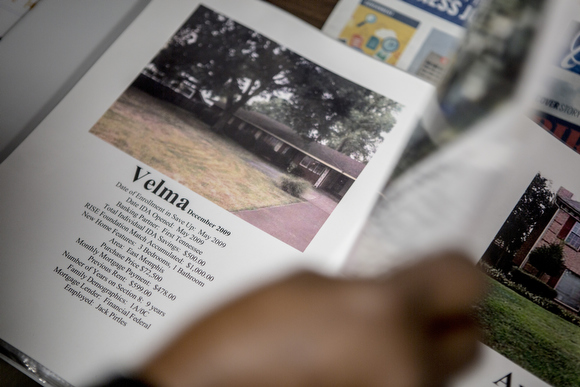

Rise’s Save Up program helps those who have completed their financial education classes buy an asset like a house to save, including a match of $2 for every dollar they save up to $1,000.

On the walls of the Rise offices are photos of homes bought through the program. New attendees are shown the wall on the first night of orientation.

“We’re saying, ‘people just like you could purchase these home,’” said Williams.

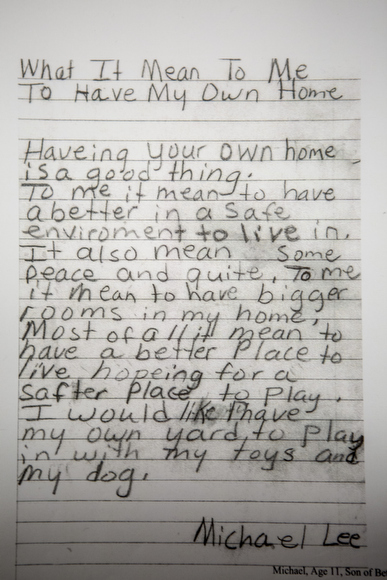

![]() A letter written by the son of a new homeowner that received help from the RISE Foundation.

A letter written by the son of a new homeowner that received help from the RISE Foundation.

This is similar to Advance Memphis’ Individual Development Account match program, which is part of a nationwide, policy-backed network of nonprofits, banks, and government agencies who sponsor programs to assist low-income people in saving for a car, home, small business, or education. Advance’s program also matches two dollars for every dollar the account holder deposits.

“Especially in Memphis, a car is vital with the poor public transportation. A lot of the good jobs are way out there and people have to travel pretty far from South Memphis…Without a car, their jobs are on the line,” Brainerd says.

Rise also has the Goal Card Incentive Program that targets students in 5th through 12th grade and incentivizes them to reach academic and financial goals through mentorship and rewards. Their National Neighbors Silver program for senior citizens teaches older adults how to avoid scams and informs them about the benefits and services available to them at their age.

“We’re empowering them to take control of their lives, teaching them new patterns and what there is to gain from making wise financial decisions—giving the gift of information.” Williams said.

For South Memphians who have been unbanked for generations, programs like these can make the difference between the increasingly-expensive cycle of poverty and predation and stability.

"Financial literacy became a new day for me,” Taylor said.

“If I would’ve known what I know now twenty years ago, I would be on a different path. But because of Rise, I know better… The more prevalent Rise is and the more the message gets out there, it’ll help people.”